What to Expect from Social Security

If you are planning on drawing on Social Security benefits to support yourself in retirement, you probably (rightly) worry about the status of Social Security benefits. This morning, the 2019 Annual Report on Social Security was released. There were no major changes from last year’s report, which is not good news since the Social Security Trust Fund is projected to run out of money.

This blog post provides highlights from the 2019 Annual Report and explains what it means for retirement planning.

Social Security: Workers per Beneficiary

Social Security provides income for retirees and the disabled. Currently, there are about 64 million beneficiaries of Social Security; 54 million are retirees and 10 million are disability recipients. Social Security is funded by payroll taxes which are assessed on the first $132,900 in income in 2019 (this cap increases every year, and is up $4,500 from 2018).

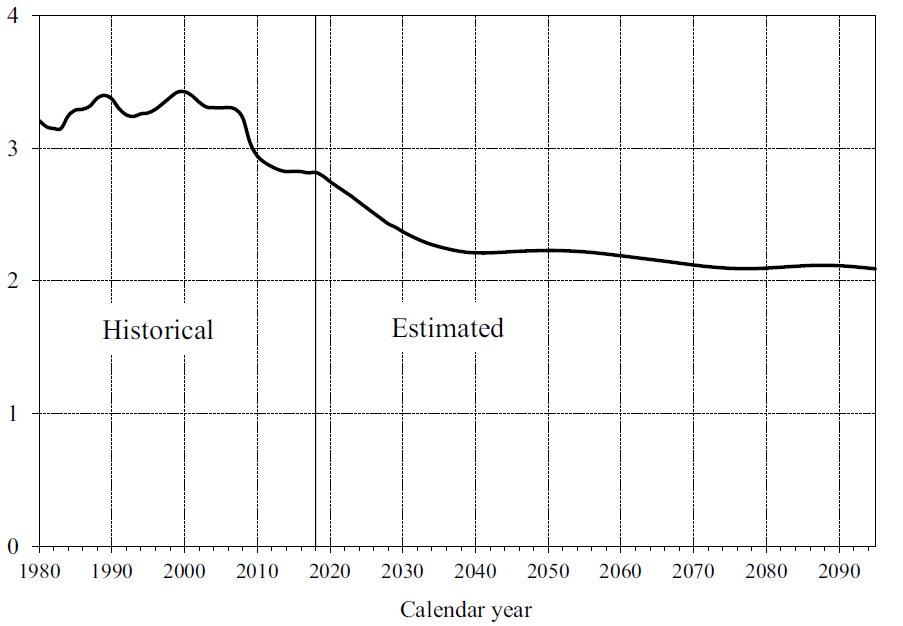

Social Security works well when the number of workers is sufficient to provide payroll tax contributions to cover the costs of benefits paid to beneficiaries. With the aging of the Baby Boomer generation, increasing life expectancy, and declining birth rates in the U.S., however, the average number of workers per beneficiary has been declining.

The chart below shows the downward trend from a recent high of 3.4 workers per beneficiary in 2000 to 2.8 today. The number is projected to fall to 2.3 in 2035.

Chart: Workers per Social Security Beneficiary: 1980-2090

The Social Security Trust Fund

During periods when there were more workers per beneficiary, excess payroll tax contributions were set aside in a trust fund to pay for future retiree and disabled persons’ benefits. (Technically, there are two funds collectively referred to as “The Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds”, but we’ll just call them the “Social Security Trust Fund” here for simplicity.)

The Social Security Trust Fund now has $2.9 trillion in assets. However, since 2010, benefits have exceeded payroll contributions. Today’s report projects that, starting in 2020, the Trust Fund will start to be drawn down. And, by 2035, the Trust Fund will be fully depleted, leaving insufficient money to pay for benefits. This means that promised levels of benefits cannot be paid out starting in 2035 without some sort of reform.

Potential Fixes to Social Security

There are numerous proposed changes to Social Security that would make the program solvent (or temporarily solvent, at least). The Social Security Administration has reviewed a number of legislative proposals, the reviews are available online. Also, in 2012, AARP published a list of proposals which can be found here.

Broadly speaking, potential fixes fall into three categories:

- Raising the retirement age,

- Decreasing benefits, and

- Increasing taxes.

If the past is any guide, we can look to 1983, the last time the Social Security Trust Fund was about to run out of money. At that time, the two primary reforms to fix Social Security (explained at length here) were gradual increases to the retirement age and increasing taxes. Cutting benefits was not a meaningful component of the reform; in some areas benefits were even increased!

Right now, there is no way to know for certain what might happen. There seems to be no political will to tackle Social Security reform now, so at Archer Row Advisory, we don’t think any reform will occur until closer to 2035. If that’s the case, then 2035 reform may mimic 1983 — with increased taxes and a gradually increased retirement age for future beneficiaries.

How to Treat Social Security in Retirement Planning

Given the future shortfall in Social Security, we suggest the following when planning for retirement:

- As a retiree, if you have other income, assume your taxes will increase. Increasing taxes on Social Security recipients with no other sources of income is probably a political non-starter. However, taxing recipients with other sources of income is a politically feasible way to reduce Social Security’s costs that was used in the 1983 reform.

- If you are planning on retiring after 2035, expect to delay receipt of Social Security. Retirement ages are increasing now due to the 1983 reform. It is likely that further increases in the retirement age will be a component of the next round of reform given that life expectancy has continued to rise.

- Expect taxes to go up, especially after 2034. The 2019 federal budget is projected to be about $900 billion and the national debt is over $22 trillion and rising. The Trump tax cuts for individuals expire at the end of 2025, and other increases may be needed to support existing levels of government spending and debt. When you add on the need to address Social Security, it seems very likely that tax rates will be significantly higher in the coming years. (This is one reason to favor Roth IRAs over Traditional IRAs, all other things being equal.)

Closing Thoughts

If you have questions about your retirement planning, call Archer Row Advisory today at (818) 539-8808 or click here to leave us a message. If you have thoughts on this post, please share them in the comments below.

Leave a Reply

Want to join the discussion?Feel free to contribute!